How Much Money Do You Need to Make to Buy a Home on the South Shore of Boston?

Purchasing a home is a big financial decision, and understanding how much money you need to make to buy a home on the South Shore of Boston is crucial. Let's walk through the various factors that influence your ability to purchase a home, including living wage calculations, lender assessments, and debt-to-income ratios. We'll also explore the median home prices in several South Shore towns to give you a clearer picture of the local real estate market. Keep in mind, whatever you budget ends up being - we can find you a home that you love! I work extensively to ensure my clients have the support they need, regardless of price point!

Understanding the MIT Living Wage Calculations

The MIT Living Wage Calculator is an interesting tool I found that provides insights into the minimum income necessary for individuals and families to meet their basic needs without relying on public assistance. This calculator considers various expenses, including housing, food, transportation, healthcare, and other necessities, to determine the living wage for different regions.

In Massachusetts, the living wage varies depending on the county and household size. For example, a Family of 4 in Plymouth/Norfolk county which makes up a lot of the South Shore needs a combined family income of $145,000.00 to have what is considered a "living wage." The living wage is an essential baseline for understanding the minimum income required to sustain a household, but it doesn't account for the additional financial commitments involved in purchasing a home, such as down payments, mortgage payments, and property taxes.

Living wage isn't necessarily the exact answer to how much you need to make in order to buy a home, it is more of a general starting point on expenses to life ratio here on the South Shore.

How Lenders Analyze Income and Debt-to-Income Ratios

When you're considering buying a home, lenders will scrutinize your financial situation to determine your borrowing capacity. Two critical components of this assessment are your income and debt-to-income (DTI) ratio.

The 28/36 Rule

The 28/36 rule is a guideline that lenders often use to evaluate your financial health. According to this rule:

- You should spend no more than 28% of your gross monthly income on housing expenses, including mortgage payments, property taxes, and insurance.

- Your total debt payments, including housing expenses, should not exceed 36% of your gross monthly income.

Adhering to this rule helps ensure that you can comfortably manage your mortgage payments without overextending your finances.

Debt-to-Income Ratio

Your DTI ratio is a crucial factor in determining your mortgage eligibility. It is calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI ratio indicates a healthier financial situation and increases your chances of securing a mortgage.

Lenders typically prefer a DTI ratio of 36% or lower, but some may consider higher ratios if you have a strong credit score or other compensating factors. It's important to manage your existing debts carefully, as excessive debt can limit your borrowing power, even if you have a high income.

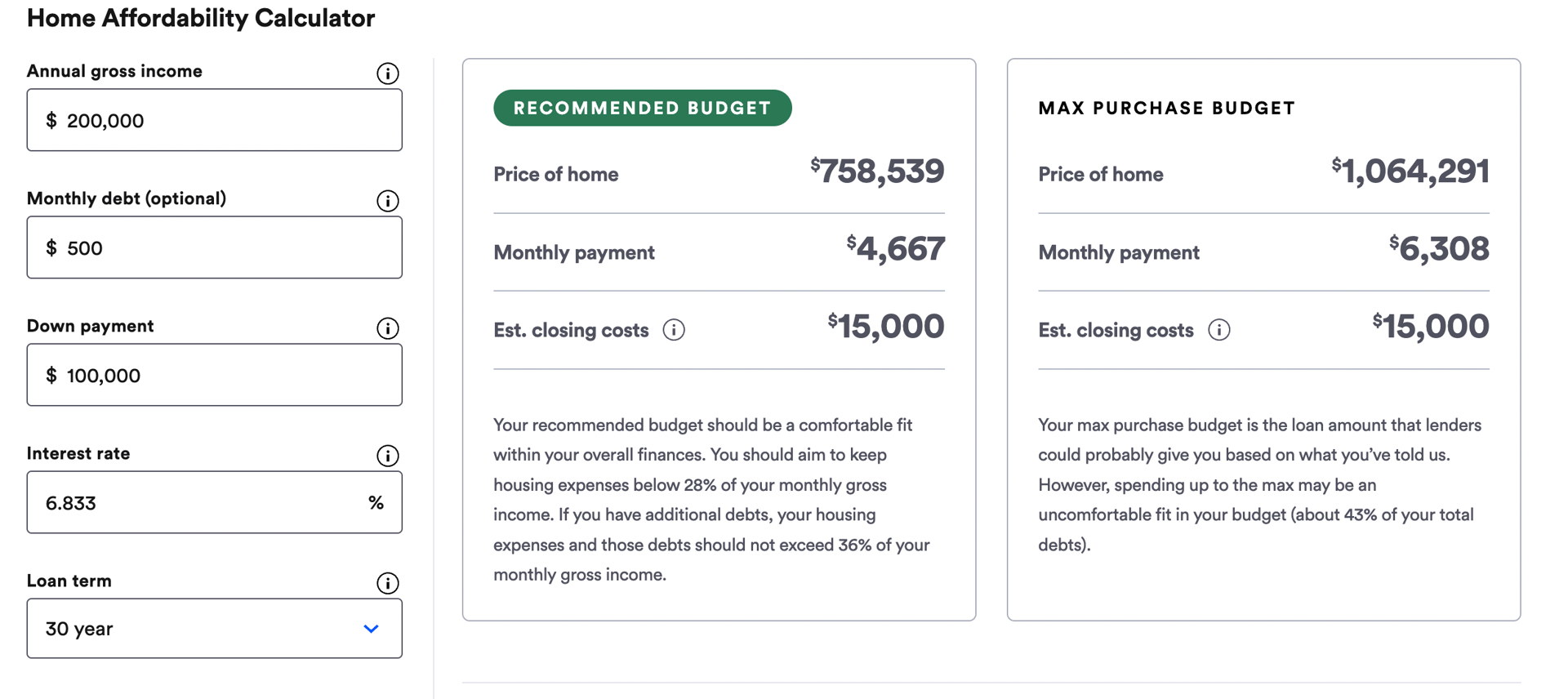

Buying Power with a Combined Family Income

Let's consider a scenario where you have a combined family income of $200,000 and can put down $100,000 as a down payment. In this case, you may be able to afford a home priced between $750,000 and $800,000, depending on your DTI ratio and other financial factors.

This estimate assumes that you have a manageable level of debt and can secure a favorable mortgage interest rate. However, individual circumstances vary, and it's essential to work with a lender to assess your specific situation. We can also get started with a general conversation to help you understand where things may stand for you and your family. Don't hesitate to reach out to me with questions.

Here's a simple example, you can see how much the budget can vary based on many factors.

Connecting with Lenders

The best way to determine your borrowing power and explore your home-buying options is to connect with experienced lenders. They can provide personalized assessments of your income, debts, and potential mortgage eligibility. If you're considering purchasing a home on the South Shore, feel free to reach out to me. I can connect you with some of the best lenders in the business to help you navigate the mortgage process. I have a lot of great connections I can put you in touch with to get started with the process.

Median Sales Prices in South Shore Towns

To give you a better understanding of the real estate market on the South Shore, here are the median home prices in several towns:

- Hingham, MA: $1,250,000

- Cohasset, MA: $1,300,000

- Norwell, MA: $950,000

- Hanover, MA: $755,000

- Weymouth, MA: $593,000

- Quincy, MA: $679,000

- Braintree, MA: $670,000

- Hull, MA: $768,500

- Pembroke, MA: $599,900

- Marshfield, MA: $727,500

- Kingston, MA: $615,000

- Milton, MA: $870,000

These median prices reflect the diverse range of housing options available on the South Shore, from more affordable homes in Weymouth to luxury properties in Cohasset. Regardless of your budget, we can get you into a home!

Final Thoughts from Hillary;

Buying a home on the South Shore of Boston requires careful financial planning and a clear understanding of your income, debts, and borrowing capacity. I can feel like an overwhelming process but I am here to help along with understanding lender assessments, and exploring local real estate prices, you can make informed decisions about your home purchase.

If you're ready to take the next step, reach out to me for personalized guidance and connections to top lenders who can help you achieve your homeownership goals. The sooner we get you in touch with a lender and figure out where you need to be - the sooner we can get you into your dream home!

[email protected] | HillaryBirchGroup.com